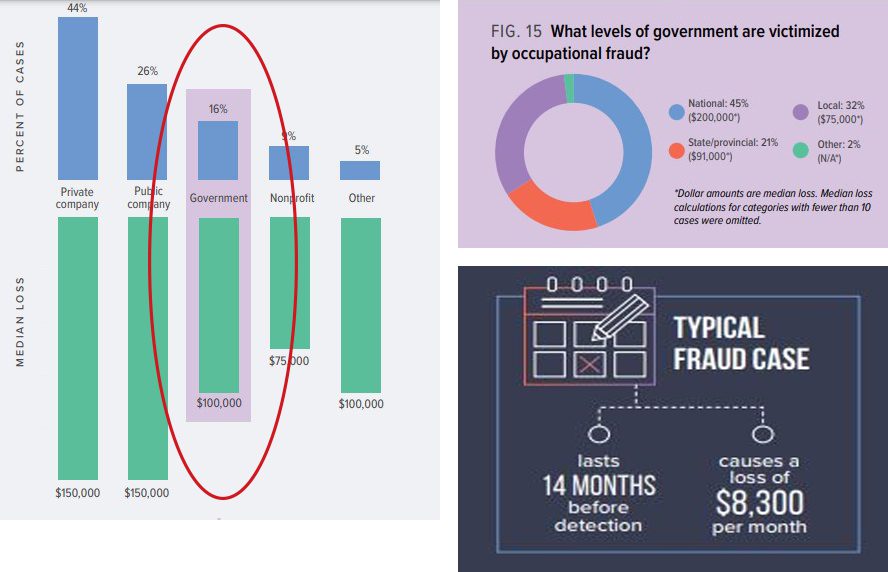

Government entities are responsible for 16% of fraud cases reported and an average loss of $100,000 per case, the third highest, according to the 2020 Report to the Nations. Fraud generally occurs in entities with weaker internal controls and minimal oversight from the elected officials. Smaller entities are at higher risk of fraud temptation due to the lack of segregations of duties.

Images from: ACFE 2020 Report of the Nations

What are temptations for employees to commit fraud?

What are temptations for employees to commit fraud?

The Fraud Triangle outlines the three elements that are typically present when an individual commits occupational fraud – Pressure, Opportunity, and Rationalization. All these elements are typically present when fraud is preformed, so effectively addressing any one of them will help minimize the fraud risk.

What are some red flags that fraud could be occurring?

- Any unusual discrepancy between actual performance and anticipated results. Examples:

- An unexpected major increase from budget in “supplies” accounts/expenses

- Unexplained decline in user fees or other revenues

- Odd transactions or discrepancies with petty cash

- Frequent and excessive adjusting journal entries

- Receipts not matching bank deposits

- Disbursements to unknown and/or unapproved vendors

- Pre-signed blank checks or one signature on checks

- Gaps in receipts or check numbers

- Consistently late reports

- Disregards for internal control policies and procedures

- Lack of basic internal controls

- Segregations of duties

- Independent checks

- Adequate records and documentations

Employee red flags

- Major lifestyle changes, living beyond means

- Refusal to take vacations

- Defensive and excessive control issues over their work

- History of large reoccurring debt

- Conflicts of interest – employee having financial benefit in vendors sending requesting payment

- Addiction problems (gambling, alcohol, etc.)

Images from: ACFE 2020 Report of the Nations

Questions? Contact our forensic accounting expert, Kari Steinbeisser, at (320) 214-2916.