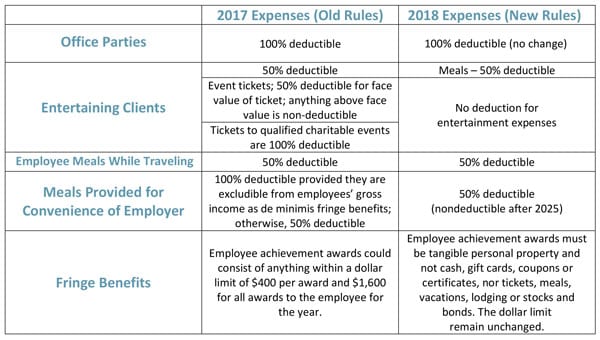

Prior to the Tax Cuts and Job Act, taxpayers generally could deduct 50% of expenses for business-related meals and entertainment. Meals provided to an employee for the convenience of the employer on the employer’s business premises were 100% deductible by the employer and tax-free to the recipient employee. Various other employer-provided fringe benefits were also deductible by the employer and tax-free to the recipient employee.

Under the new law, for amounts paid or incurred after December 31, 2017, deductions for business-related entertainment expenses are disallowed. Meal expenses incurred while traveling on business are still 50% deductible, but the 50% disallowance rule will now also apply to meals provided via an on-premises cafeteria or otherwise on the employer’s premises for the convenience of the employer. After 2025, the cost of meals provided through an on-premises cafeteria or otherwise on the employer’s premises will be nondeductible. Businesses should keep the new rules in mind as they plan their 2018 meals and entertainment budgets.

Tax Saving Tip: Maximize tax deductions and save time on tax preparation for 2018 by setting up separate general ledger accounts for business meals (50 percent deductible), entertainment/amusement (nondeductible), and recreational/social employee expenses (100 percent deductible).